PCB, Flex & PCBA Cost Pressures in 2026: What OEMs Need to Watch

Nguyen Tran2026-04-07T16:52:12+00:00Electronics manufacturing is heading into 2026 under pressure from several directions at once. Rising metals costs, laminate and prepreg repricing, labor shifts in key manufacturing regions, foreign exchange movement, and tighter capacity tied to AI and data-center demand are all contributing to higher PCB, flex, and PCBA costs. For OEMs, that is creating shorter quote validity windows, more frequent re-quoting, and less predictable lead times.

That is why PICA Manufacturing Solutions created the white paper, PCB, Flex & PCBA Cost Pressures in 2026: Data, Drivers & Practical Mitigation. The paper explains what is driving the market and gives engineering, sourcing, and operations teams practical context for reducing risk before cost pressure turns into program disruption.

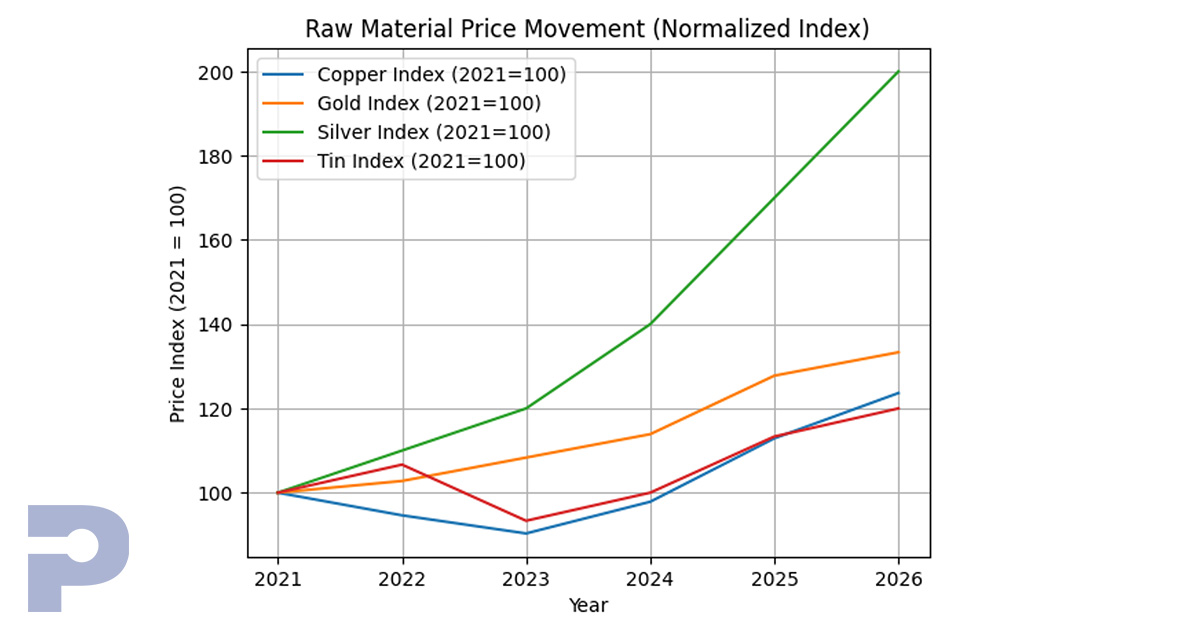

One of the largest cost drivers is raw material pricing. Gold, copper, tin, silver, and nickel all affect PCB fabrication, flex circuit production, plating chemistry, solder materials, and surface finishes. Gold and silver increases can put pressure on ENIG, hard gold, RF, sensor, and medical applications, while copper remains a major factor for multilayer and heavy copper designs. At the same time, FR-4, copper-clad laminates, prepregs, and polyimide materials are also under pressure, especially in flex and rigid-flex manufacturing.

Facing rising PCB, flex, and PCBA costs in 2026?

Download the white paper for practical insight on reducing risk, controlling costs, and improving sourcing strategy.

Labor and regional cost changes are adding to the challenge. Tightening labor conditions and wage pressure in China continue to affect manufacturing costs, while currency movement can influence supplier pricing models. On top of that, AI and data-center demand are pulling on upstream PCB material and fabrication capacity, which can create indirect cost pressure even for more standard products.

As these forces move through the supply chain, customers are seeing real operational changes. Quote validity windows may shrink from 60 to 90 days down to 15 to 30 days. Lead times can become less predictable, particularly for specialty materials and flex circuits. High-layer-count and advanced HDI programs may also require earlier scheduling as capacity becomes tighter.

During periods like this, many organizations make the mistake of focusing only on the lowest unit price. That can ignore the costs tied to re-spins, scrap, rework, expedite fees, inventory carrying costs, engineering time, and supply disruption. In many cases, the lowest quoted price is not the lowest total program cost.

A total cost of ownership approach gives teams a better way to evaluate suppliers. Instead of looking only at piece price, it considers the full cost of a sourcing decision across the life of a program. That broader view can help reduce risk, protect schedules, and avoid downstream costs that are far more expensive than a slightly higher initial quote.

PICA’s white paper also outlines practical mitigation strategies, including earlier engineering involvement, design-for-manufacturability collaboration, diversified sourcing, and multi-region manufacturing flexibility. In a market shaped by material inflation, labor shifts, and capacity constraints, proactive planning can make the difference between reacting to volatility and staying ahead of it.